Your Annual Insurance Review

A simple, steady way to protect your solo life

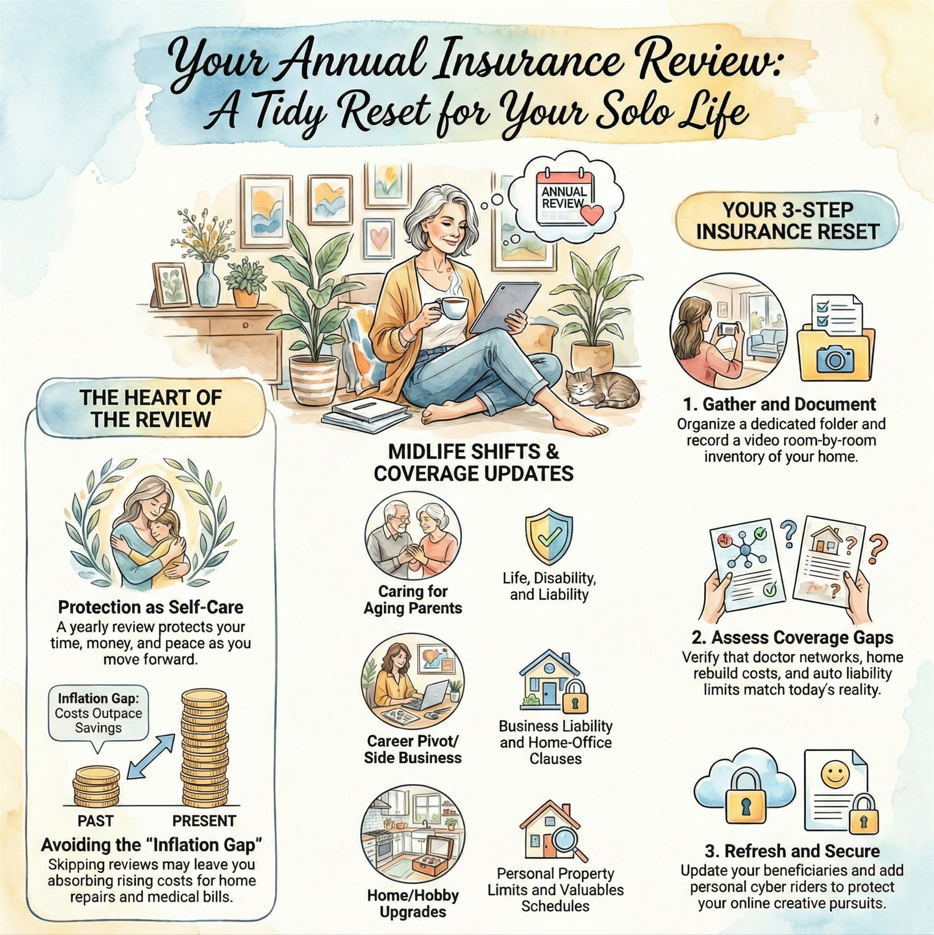

The Heart of It: An annual insurance review is more than paperwork. It’s a loving act of self-care that protects your time, your money, and your peace. You deserve clear coverage that supports your next chapter.

You carry a lot, and you carry it well. Still, it’s fair to ask if your insurance still fits your solo life now that the house feels different and the calendar looks lighter. Have you checked your policies lately?

An annual insurance review helps you see what you actually have, what you truly need, and what no longer serves you. It can lower costs, close gaps, and give you firm ground to stand on. You get to feel ready, not worried.

If you’re over 45, living on your own, or easing into an empty nest, your needs have shifted. Maybe you’ve downsized, started a side business, or now travel to see your kids. Your coverage should match today, not last decade.

Do I really need to review my insurance every year if nothing big has changed?

Yes. Even when your life looks the same, prices, deductibles, coverage limits, and insurer rules often change quietly. A short annual review helps you catch those shifts before they cost you time, money, or peace of mind.

Doing an annual insurance review will help you make calm, clear choices. You’ll spot the must-check areas, plan your next steps, and feel more secure about your life and money. No panic, just steady care for the woman you are now.

Why Your Annual Insurance Review Builds Lasting Security

Security isn’t a one-and-done. It’s a habit. A yearly review keeps your coverage in step with your actual life so a surprise doesn’t turn into a crisis. You look at what changed, adjust a few lines, and move on feeling grounded.

That’s lasting security, not luck. It’s your quiet way of saying, I take care of me.

I don’t hunt for paperwork. I keep a dedicated, clearly labeled insurance folder in my important documents file box so reviews are straightforward and contained.

A gift for you!

Life Security Essentials Organizer

Get your essential info organized with calm confidence one small step at a time

Spotting Life Changes That Affect Your Coverage

Midlife brings shifts that ripple through your coverage. If you don’t name them, you miss simple updates that protect your time and money.

- Aging parents: If you now help with caregiving or funds, review your life, disability, and liability coverage. Add medical power of attorney and check beneficiary details.

- New diagnoses or medications: Revisit health and disability policies, refill emergency funds, and note network changes. Look at riders for critical illness if offered.

- Career pivot into creativity: Freelance work, a studio, or selling art may require business liability, equipment coverage, or a home-office clause.

- Home or hobby upgrades: E-bikes, camera gear, or kitchen refreshes can exceed personal property limits. Schedule valuables and confirm replacement cost, not actual cash value.

A quick scan each year keeps your policies aligned with reality, not last year’s guess.

The Hidden Costs of Skipping Your Review

Picture this: a home repair after a storm catches you off guard. You discover your deductible doubled, and your roof is underinsured. That gap comes straight out of your pocket.

Or maybe you get a minor injury, then learn your high-deductible plan changed, and the urgent care bill stings.

Skipping a review can mean paying more for less. Building materials, car parts, and medical bills keep climbing. Insurers adjust premiums and terms to match those costs. If you don’t update limits and deductibles, you absorb the inflation.

Stay ahead with small checks that prevent big pain. Confirm replacement cost on home and auto, raise liability if you host or travel more, and keep receipts for new gear. A 20-minute review now saves you from expensive surprises later.

What if reviewing my insurance makes me anxious and I avoid it?

That’s common, especially if paperwork has felt overwhelming in the past. Start by reviewing just one policy or confirming one detail, like your deductible or beneficiary. Progress here isn’t about finishing everything at once. It’s about staying engaged enough that nothing drifts out of date.

Your Simple Step-by-Step Guide to an Annual Insurance Review

Think of this as a tidy reset. You’ll walk through a few simple steps, close small gaps, and get your paperwork to match your life right now. No drama, just calm order.

I don’t rely on notes. I keep a one-page insurance summary with key details of each policy and update it at every review. That’s what makes the information usable.

1. Gather Your Documents and Contacts

Pull out that folder you’ve been meaning to sort. Lay out policy statements, ID cards, renewal notices, and any riders. Add agent and claims contacts, account and policy numbers, VINs, and your mortgage or lease.

Snap photos and save PDFs in a cloud folder named “Insurance” with the current year. Use simple file names like “Home_policy_renewal_MMMYY.pdf.”

*MMM=Month, YY=Year, for example DEC26 for December 2026.

Share read-only access with a trusted person. Add renewal dates, license expirations, and rate review reminders to your calendar. Keep a list of beneficiaries and emergency contacts together.

Take a quick video inventory of each room and store it with your documents. Be sure to talk through what you see and open any drawers or cabinets that contain anything important you want to capture.

2. Assess Coverage Gaps and Updates

Start with health. Are your doctors still in network? What’s your current out-of-pocket max? If premiums rose, would an HSA plan make sense, or do you need richer copays while managing a new diagnosis?

Next, review your home. Do your limits match today’s rebuild costs? Add water backup or equipment breakdown coverage if your home’s systems are aging. Schedule jewelry, cameras, or art. Raise liability to $300k or higher if you host or pet sit.

Then check life and income coverage. Do beneficiaries match your wishes? Consider term life to cover debts and ask about long-term care riders.

For auto, make sure your policy covers your electric bike, rentals, or roadside needs. If you’ve upgraded your car, review gap coverage and your deductible.

3. Avoid Common Pitfalls

A clean checkup avoids the simple mistakes that cost you later. You’re not starting from scratch, you’re refining what already protects you. Think of this as a quick tune-up for your solo life.

Every December, I have a standing calendar reminder to do a quick annual insurance review. Nothing fancy, just a deliberate pause to check three must-have things: coverage, beneficiaries, and any life changes that might have slipped in over the year. I treat it like maintenance, not a crisis. I’ll be honest: sometimes the review spills into the new year. And that’s fine. What matters is having a repeatable system that brings me back to it every year, so nothing quietly goes outdated while life keeps moving.

Overlooking Beneficiary and Lifestyle Updates

Life shifts, and your paperwork needs to keep pace. Your ex might still be listed, it happens. Update to reflect who you trust today, not who made sense ten years ago.

If you’re living more mindfully, spending less, traveling more, or keeping your circle small, update how benefits flow and who gets called first.

Simple steps to make it clean:

- Pull a list of all policies: life, retirement accounts, pensions, HSAs.

- Confirm primary and contingent beneficiaries by legal name.

- Remove outdated names and add trusted backups.

- Add your current contact information.

- Update addresses for you and beneficiaries.

- Include a charity only if it still fits your values.

- Save confirmations in your current year folder.

Ignoring Emerging Risks Like Cyber Threats

As you explore new creative pursuits online, protect yourself. Scams increasingly target women who buy classes, sell art, and manage finances on a laptop.

A breach can expose bank data, tax IDs, or your shop’s customer list. Treat cyber protection as part of life security, just like smoke alarms and seat belts.

What to check and add:

- Ask your home insurer about a personal cyber or identity theft rider.

- Enable multi-factor authentication on bank, email, and social accounts.

- Use a password manager and unique logins for payment tools.

- Confirm your business or hobby policy covers online sales and client data.

- Keep receipts and serial numbers for devices in your inventory.

- Set alerts on your bank and credit files so you catch suspicious activity early.

Steady Confidence for the Year Ahead

You just gave your future self a gift. A simple annual insurance review protects your time, your cash flow, and your peace. You named what changed, tightened a few details, and built a clearer path for your solo life. That’s real security, not guesswork.

Keep it personal and light. Update limits to match today’s prices, refresh beneficiaries, and add small riders only where they serve you. Keep your folder tidy, your contacts current, and your video inventory saved.

You’re not aiming for perfect here, you’re building steady confidence. Doesn’t it feel good to know you did this on purpose?

I don’t overthink it. I schedule the review, work the list, and close it out. Done is better than delayed.

Key Takeaway

An annual insurance review is a form of self-care, not a financial chore. It protects your independence and your peace.

Small life changes can quietly create coverage gaps if you don’t revisit your policies.

A simple, repeatable system matters more than perfection or timing.

When your insurance matches your real life, you move through the year with more confidence and fewer surprises.

3 Ways to Start Today

- Schedule 30 minutes this week for your policy check.

- Call your agent for a quick chat about limits and deductibles.

- Jot down one life change to discuss, like a move or new gear.

So . . .

what’s one small step you could take today to feel more secure and supported for the year ahead?